RBI strengthens mis-selling norms, full refund if proven – The Times of India

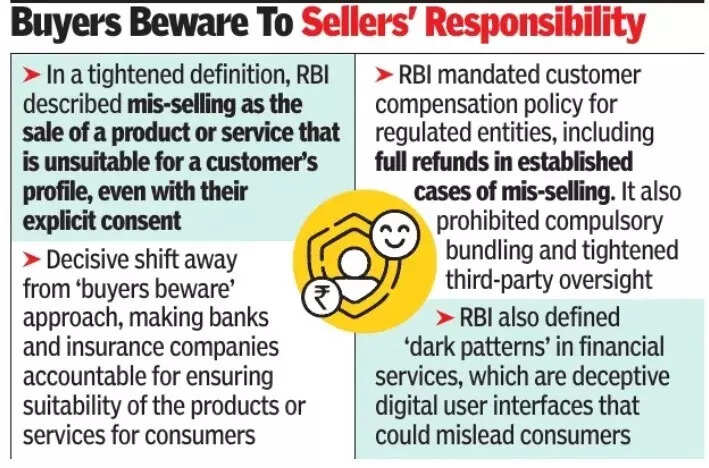

MUMBAI: Reserve Bank of India (RBI) has sharply tightened the definition of mis-selling, removing one of the biggest defences used by banks and insurance companies that the customer had explicitly consented by signing documents. Under the new framework, regulated entities will also have to make full refunds in cases of proven mis-selling.In the Draft Reserve Bank of India (Commercial Banks – Responsible Business Conduct) Amendment Directions, 2026, RBI has defined mis-selling as the sale of a product or service that is inappropriate for a customer’s profile-age, income level or risk appetite, even if the customer gave explicit consent. The central bank has also, for the first time, defined “dark patterns” in financial sales. These refer to deceptive user experience designs on digital platforms that mislead or trick customers into actions they did not intend, by impairing their autonomy or choice, and amount to misleading advertising, unfair trade practices or violation of consumer rights.

For years, banks and insurers have followed a buyer-beware approach, often citing signed fact sheets and confirmation calls to defend themselves in disputes, particularly in cases involving complex insurance or investment products sold to senior citizens. By stating that customer consent does not legitimise an unsuitable sale, RBI has effectively held banks to the principle of utmost good faith, making them accountable for the appropriateness of products they distribute rather than treating them as mere commission-driven intermediaries. RBI has also indicated that regulated entities must have a policy in place for customer compensation, including full refunds in established cases.The draft rules further prohibit compulsory bundling, making it clear that loan approvals cannot be linked to the purchase of insurance or other financial products. They also tighten oversight of third-party agents, requiring banks to display updated lists of all Direct Selling Agents on their websites and ensure that agents operating within branches are clearly distinguishable from bank employees.Industry executives said the norms, scheduled to take effect from July 1, 2026, are likely to major overhaul in the way insurance and investment products are sold through bank branches.